[ad_1]

The economic calendar is a big one, compressed into a holiday-shortened week. There are no reports scheduled for Tuesday, and I have a suspicion that the A-Teams may be a bit slow in returning to work. With the big news coming at week’s end, and the need for fresh copy on Tuesday I expect the punditry to be asking:

What should we worry about it 2018?

Last Week Recap

In the last edition of WTWA I speculated that the collected punditry, mostly the B teams, would be trying to sort out the impacts of the tax law. That was indeed the main story, but there was more speculation than substance on the tax bill impacts.

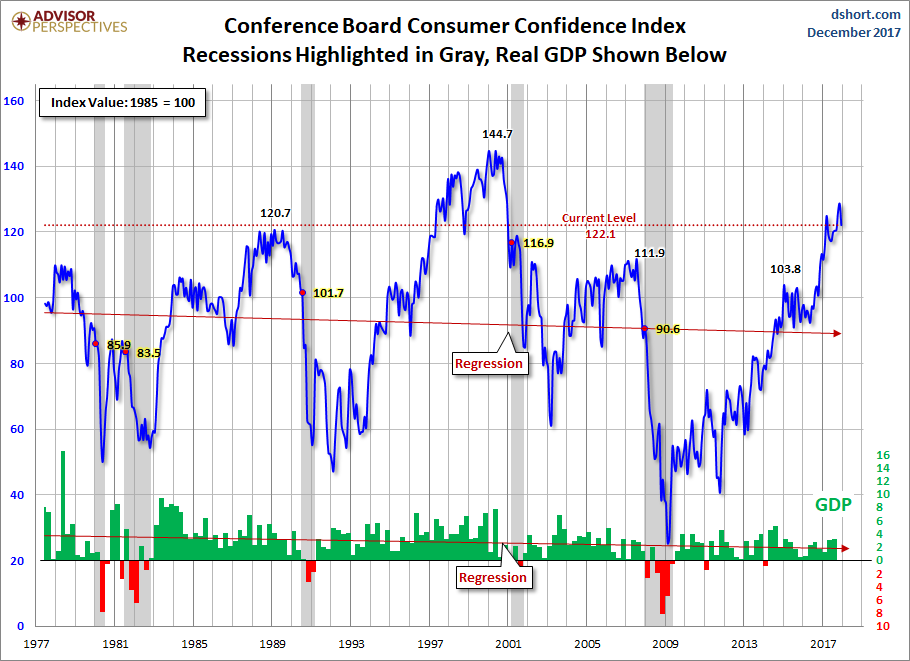

The Story in One Chart

I always start my personal review of the week by looking at a great chart. I especially like the Doug Short design with Jill Mislinski updates and commentary. You can see many important features in a single look. She takes special note of the absence of Santa Claus. The entire post is well worth reading for the collection of charts and analytical observations.

Once again, the trading range for the week was a fraction of a percent. The heavy volume in Friday’s late decline was the only notable move of the week. During Tuesday’s trading Art Cashin, in his regular appearance from the NYSE floor, quipped that coming in that day was a “waste of carfare and a clean shirt.” You could say much the same for the rest of the week.

The News

Each week I break down events into good and bad. For our purposes, “good” has two components. The news must be market friendly and better than expectations. I avoid using my personal preferences in evaluating news – and you should, too!

The economic news was very light, mixed, and mostly ignored.

The Good

- Chicago purchasing managers index spiked several points to 67.6, handily beating expectations.

- Pending home sales increased 0.2%. While this is a decline from the prior month gain of 3.5%, expectations were for a loss of 0.7%.

The Bad

- Consumer confidence dipped to 122.1 from a prior of 129.5 and missing expectations of 128. One question for the new year will be how to interpret data which is “less good” but historically strong.

Jill Mislinski’s report places this report “in context.”

- Initial jobless claims were unchanged at 245K, but a decline to 238K was expected.

The Ugly

Dr. Phil? Since I have never watched his show, I would not have recognized him on the street until I saw the pictures in these articles on Stat (here and here). I had heard of him along with Oprah connection, and had a generally favorable impression based upon little real information. As a quick path to knowledge, I turned to a reliable source, Mrs. OldProf. Looking up from her “Words with Friends” game (you had better play well if you challenge her) she informed me that she never watched his show. Despite this, she seemed to have a positive impression from the Oprah days but said that he had “gone commercial” when he got a spinoff. Information is acquired in many ways, and she was more interested in her competition than in providing footnotes!

It is especially sad when we are disappointed by those who are supposedly providing help. Someday, but not today, I will further explore the theme of media and social policy.

The Week Ahead

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react.

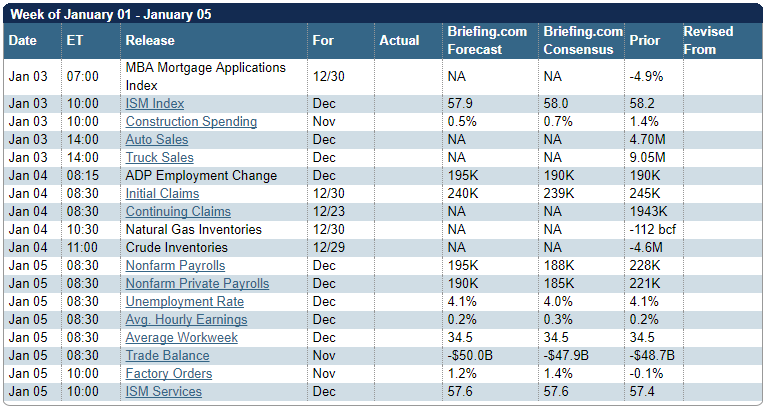

The Calendar

The new year starts with many of the most important reports in a holiday-shortened week. The ISM indexes (both manufacturing and services) and auto sales. Most important of course, will be the employment report at week’s end and the ADP private employment release on Thursday. I don’t expect anything important from the FOMC minutes to be released Wednesday.

Briefing.com has a good U.S. economic calendar for the week (and many other good features which I monitor each day). Here are the main U.S. releases.

Next Week’s Theme

Once again there is a short trading week, but this time it is loaded with economic reports. Some market participants might miss Tuesday trading as well, and the week’s news is back-loaded. The analysis of the tax legislation is still a work in progress. Those needing to fill space over the next few days are most like to be turning to the year ahead. With plenty of forecasts already logged, I expect a more negative focus with many asking:

What could derail markets in 2018?

Thanks to readers who nominated candidates for a 2018 list of worries. I have combined these suggestions with those drawn from polls and some popular sources. In a change from my regular format, I will emphasize this list of concerns. In each case I will offer a brief statement (in italics) of my own current assessment. I cannot do a complete analysis of every current problem, so we might think of this as an agenda – items that require more analysis or attention throughout the year. This approach is especially useful to my own planning. I hope readers also find it helpful.

My analytical framework includes the following steps:

- Is this a “market” issue or a problem without impact on the economy or corporate earnings?

- Can we estimate the significance? Even a rough approximation is often helpful.

- How likely is this problem to occur during the next year?

- Can we quantify the likely effect?

- Is it a long-range problem that requires immediate investment action?

- Is it a problem where we can prepare and monitor danger signals?

- Is there a good way to hedge investments against this concern?

A Helpful Classification

Economy

Inflation rates the cover on this week’s Barron’s. Even a small increase in prices can have a significant effect on bonds. Historically, higher inflation is associated with lower P/E multiples.

This is an argument that seems to be used to fit any author’s convenience. Some note that the Fed’s inflation target has not been reached, taking it as a sign of weak growth. Others have predicted (ever since 2010) that we were due for hyperinflation. Thinking clearly, we would like modest inflation and strong growth. If we can get the growth without a lot of inflation, that is desirable. If inflation is accompanied by stronger growth and better earnings, it is bad for bonds but not for stocks. This context is missing in everything I read.

Recession is a perennial forecast for many. After creating many home-made indicators, there is some attention to the yield curve. The current obsession is tracking every small flattening in the curve, with an emphasis on what might happen next. (Eric Parnell).

In 2010, I identified the best real-time recession forecaster, Dr. Robert Dieli. The yield curve is part – and only part – of his approach. He also monitors many coincident indicators for confirmation. In addition, I review and publish regularly the best work on recessions.

There is no reason to worry about modelers and pop economists who have tweaked past data to prove a point. As Dr. Dieli recently noted, they are trying to forecast the indicator, not the recession.

The dollar – declining or stronger. Critics worry about either.

How does one analyze a moving straw man?

Debt – of all types. Government, corporate, and individual. The argument about debt generally compares current levels to the past and asks what would happen with higher rates.

For individuals, most debt and debt service has improved. Student debt is a separate and important issue. Corporate debt does not worry me. Corporations have chosen to finance activities with low-interest, low-cost loans rather than by selling equity. This is a logical choice. Government debt is a very different issue. As the economy has gotten stronger, deficits as a % of GDP or tax revenues should get lower. Future commitments should be seriously analyzed. State and local governments must address pension plans.

The government debt problem is nearly impossible to address without bipartisan effort. Otherwise, it is too easy to point fingers.

This a serious problem, but probably not an immediate threat for markets.

Market Characteristics

Valuation. The consensus that equities are overvalued is so strong that it gets a brusque summary, not analysis. Mark Rzepczynski, for example, sees a consensus prediction of a 6% stock gain for 2018 as a sign of (unjustified?) optimism.

The traditional valuation indicators look at the history of P/E ratios. There is no comparison of potential investment gains to bonds or to expected inflation. Most of the data in the analysis is irrelevant, drawn from past epochs with little similarity to current circumstances.

Indicators “rolling over.” Any time an indicator looks “less good” it will draw attention. Growth at a declining rate will be described as “growth is weakening.”

This will happen, and it might start soon. The rate of improvement cannot increase forever, even if conditions remain sound. This type of analysis will provide confirmation bias, but it should not be a concern. It may have a temporary effect on market psychology, but not on stock fundamentals. Forewarned is forearmed on this one.

Earnings stall. A long-running argument is that profit margins are too high and will eventually revert to the mean. This has been a frequent argument for many years.

I expect profit margins to see a gradual decline as the economy improves. This naturally brings in more competitive pressures. This will be a negative effect on earnings, but offset (how much?) by economic improvement. We do not need to jump the gun on this oft-repeated concern. We’ll be able to monitor it in real time and note any offsets.

Bitcoin. There is no shortage of pundits who see Bitcoin as a bubble and a market threat. Here is an example (Fortune).

Since there is no way to value Bitcoin on the fundamentals, one cannot say if it is a bubble. The rapid increase in value might be recognition of a new, much needed, product/service. Even it if is a bubble, the implications for other markets are not clearly established. It is something to monitor, observing the apparent relationships.

US politics and policy

Mueller investigation. While the Administration currently expresses no interest in firing Mueller, many lack confidence in that assurance. A worst-case scenario foretells a Watergate-like situation, with government crippled and many new worries.

The direction of the investigation, and the response, is one of the big unknowns for 2018. While the effect on the economy is difficult to gauge, we know that markets, hating uncertainty, will be skittish. It seems like a concern to monitor, not one for advance hedging.

Mid-term elections. A fractious Congress could stall legislation that would be helpful for the economy as well as people in need. Bloomberg sees the parties as “spoiling for a fight.”

This is likely, important, and probably unavoidable. We might have a window of opportunity at the start of the year. We will also get some early signals of possible cooperation. Some representatives might choose not to run on a platform of obstruction and/or blaming the opposition. Perhaps I am too optimistic about this, but we can watch it very closely as the situation develops.

Trade policy. Much of the multi-decade economic expansion has resulted from free trade. Ending these relationships will spark inflation and retaliatory measures.

This is a real concern. To the extent that measures are within the power of the President, some have already occurred. While the negative effects may not be clear to a non-economist, we can expect plenty of reaction from groups traditionally supporting Republicans as well as those on the fence.

I am not sure how this will play out. It is an important theme to monitor, with potential effects on the overall economy as well as particular sectors and stocks.

Government shutdown. This would create some immediate economic impact, but also a signal about cooperation and future policy.

I expect a shutdown to be avoided, even if it requires some concessions to Democrats.

The Fed. Somehow the Fed will bungle the exit from QE. The chickens will come home to roost, etc.

This is the last refuge of the Fed bashers who have been wrong for years. The roll off of securities is very modest, especially taken in the context of daily Treasury trading volume.

Global politics and policy

Middle East. There seem to be increasing tensions on many fronts. Traditionally, this has led to higher oil prices, a “tax” on the US economy with no benefit from expenditures.

Middle East conflict remains a policy concern, but less of a market concern. The “latent capacity” from fracking in known US oil fields has restrained the threat of higher oil prices.

N. Korea. Irrational action could start a conflict in the region or more broadly. We cannot know whether the modern “rules of engagement” will prevail.

This is a very real threat, especially since US policy seems so ill-defined. There is no effective way to hedge this threat on a long-range, general basis. If the potential for conflict increased, there are several preparatory steps. I am researching these, and others should as well.

Iran. A similar situation to N. Korea.

The UN restrictions are supported by nearly everyone except the US. No one can really know where this policy initiative is going. Once again, there is no clear investment response.

Disasters and Events

Terrorist attacks, both in the US and abroad.

We cannot predict when a specific attack will occur, but we know they will happen. This is a very sad story, but (so far) not a market story).

Wars seem to have increased in frequency, sometimes involving important powers.

Once again, this is certainly true. The market effects seem to be lower than at the time of the Gulf War, for example. My intention is to monitor these situations closely, with special attention to impacts on financial markets and particular sectors. I do not see it as a reason for a complete market exit.

Hacks and glitches. These are a bigger risk as trading procedures have embraced more automation. (24/7 Wall St covers this, and nine other worries!)

This is a valid concern, something that is both a high probability and important. Attacks could focus on trading, the IRS, sensitive government information, or many other places. Our desire to save money has left a high level of vulnerability in government computer systems, including local government.

I own some stocks that fight these attacks, but I have no illusion that this is a sufficient hedge. This topic deserves much more attention.

While this may seem like an extensive list, there are some key ideas left out. I’ll have more in the Final Thought.

Quant Corner

We follow some regular featured sources and the best other quant news from the week.

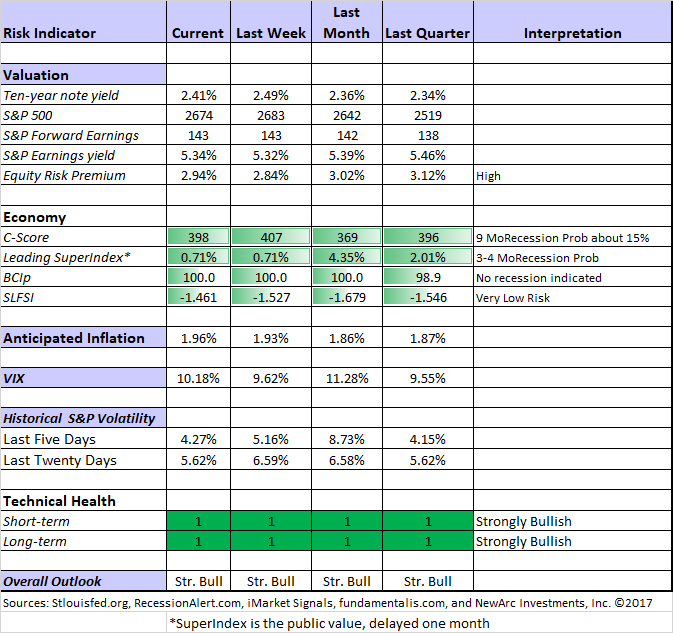

Risk Analysis

I have a rule for my investment clients. Think first about your risk. Only then should you consider possible rewards. I monitor many quantitative reports and highlight the best methods in this weekly update.

The Indicator Snapshot

Recession odds remain low and many economic indicators are improving.

A client is curious about my rating of the Equity Risk Premium as “high.” Good question! I use the inflation rate as part of the comparison, a method that has been quite effective. Many economic indicators seem to be at an extreme when viewed in isolation, and quite different when adjusted for inflation. When the ten-year note was at 14%, for example, what would you have expected stock returns and the ERP to be?

Looked at another way, stocks carry a premium because they are viewed as more dangerous. With dividend yield close to the Treasury return, and inflation expectations edging higher, which do you think is riskier?

The Featured Sources:

Bob Dieli: Business cycle analysis via the “C Score.

RecessionAlert: Strong quantitative indicators for both economic and market analysis.

Brian Gilmartin: All things earnings, for the overall market as well as many individual companies.

Georg Vrba: Business cycle indicator and market timing tools.

Doug Short: Regular updating of an array of indicators. Great charts and analysis.

Insight for Traders

Our discussion of trading ideas has moved to the weekly Stock Exchange post. The coverage is bigger and better than ever. We combine links to trading articles, topical themes, and ideas from our trading models. This week’s post takes up a crucial question: When should you exit a trade? Model performance updates are published, and of course, there are updated ratings lists for Felix and Oscar, this week featuring the Russell 1000. Blue Harbinger has taken the lead role on this post, using information both from me and from the models. He is doing a great job, presenting a wealth of new ideas and information each week.

Insight for Investors

Investors should have a long-term horizon. They can often exploit trading volatility!

Best of the Week

If I had to pick a single most important source for investors to read this week it would be this article on “the resulting fallacy.” Author Stuart Firestein is a professor of neuroscience at Columbia. His interview subject, Annie Duke, could have become an academic but instead became an expert at poker with more than $4 million in winnings. “What does this have to do with investing?” you might ask. If you read the interview carefully, you will see. One of the most difficult challenges in helping investors is to rip them out of the anchoring and confirmation bias of traditional investment news.

Suppose someone’s model suggests a 73% chance of recession in the next year. (Or a certain candidate winning an election, etc.) The recession does not occur. Does that mean that the prediction was incorrect?

That is the conclusion reached by most and promoted by many who want to diminish expertise in all fields. You can identify a real expert if the source focuses on the process and the results over many, many instances. Many is much more than most people think.

As someone who has played and enjoyed all three “mind games,” I note that the same principle is at work in bridge and backgammon. The “best” play does not always work. And of course, this is significant crossover in experts in all of these activities, as well as with successful investors.

Stock Ideas

I’ll have the usual collection of stock ideas next week. For now, I suggest investors join me in reading selections from the first-rate Seeking Alpha Positioning for 2018 series. There are many good ideas.

Personal Finance

Seeking Alpha Senior Editor Gil Weinreich continues his strong work. Every day he has a topic of interest for financial advisors. It usually hits key points for individual investors as well. This week he drew upon an interesting psychological study with implications for your personal finances.

Watch out for

Analyst stock ratings. Citigroup was fined my FINRA for sending false stock ratings to retail customers. Buy instead of Sell, for example. And vice-versa. The fine was $11.5 million. Wow! For the record, in my “Great Stocks” program I use analyst ratings as a contrary indicator, buying Apple (AAPL) when it was hated and selling when CNBC could not find a negative analyst to feature.

Final Thoughts

Here are two final thoughts.

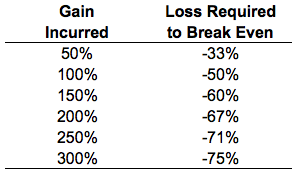

1. The list of worries has a dog that is not barking: upside risk.

I have raised this topic in twenty or more posts, but you do not see it discussed very much. I was pleasantly surprised at this Ben Carlson post where he handles the question nicely. Sound investing requires a balanced approach. He includes the flip side of a common chart on risk and recovery:

He concludes as follows:

But investors who focus exclusively on downside protection without a plan for how to handle the upside will be sorry. No one really views upside in the markets as a risk but it certainly can be a risk if you miss out on large gains or have no plan of attack for how to handle them.

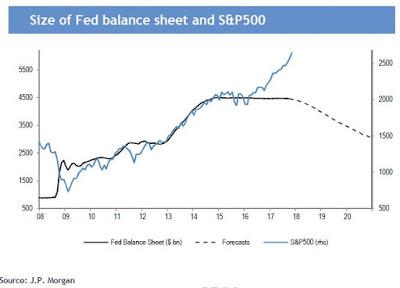

2. Worries are positive for the market. The sweet spot for the long-term investor comes when most market participants are needlessly worried about issues you can see with clarity if you try. This is nearly always the case. It is the foundation of the generally misunderstood “wall of worry” concept. There is a very long list of expired worries. Cam Hui points out a multi-year favorite, the Fed balance sheet (always described by critics as “bloated.”)

There is nothing more positive for investing than a long list of well-documented worries!

[Need a year-end tune up for your portfolio? This is the time to schedule a free consultation, read my paper on the top investor pitfalls, or both. If you are concerned about major declines, you might be interested in my paper on risk. Just write for our free information on these topics. While they describe what I am doing, the do-it-yourself investor can apply the same principles. Both the concepts on recessions and how we used it to forecast Dow 20K are available for free from main at newarc dot com].

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

[ad_2]

Source link